Asigură-te

că ai instalat

deja

aplicația de

mobile

banking

Beware of fake calls! ANAF, the bank or other authorities do not ask you to provide bank details or access codes, nor to access various links, which may lead to the installation of remote control applications on your computer. Do not perform "test banking transactions" and do not accept such requests received by phone, it may be a fraud! Contact your banking advisor immediately and report suspicious situations!

×Daily banking

YOU

SMS banking

The remote banking service provides you with information on your bank accounts directly from your mobile phone.

MyBRD Contact

MyBRD Contact is a service which allows you to quickly make your current operations through the phone.

Other services

Saving and investments

Offers

SME<sup>1-50M Euro</sup>

Online trading

Other services

Our team

Depository services

Safekeeping, registering, monitoring and controlling the applications for subscription or redemption of fund units.

Issuer services

Distribution of fund units, dividends and bond payments. Group distribution services within public offerings.

Global and local custody services

Administration availability of customer accounts to their instructions - financial instruments operations or cash.

Clearing services

Clearing services for transactions made on Bucharest Stock Exchange, Bucharest Clearing House and SIBEX.

Contact

Clearing services for transactions made on Bucharest Stock Exchange, Bucharest Clearing House and SIBEX.

News

News and related materials of our current activity: from business press releases to cultural, educational, sport or technological projects

Scene 9

is an online cultural publication that shapes the portrait of the new generation of creators

Școala 9

is an editorial project dedicated to the pre-university education created by DoR and BRD

Culture

We invest in culture because we need leaders and projects to remind us where we come from, who we are and where we are heading to.

Education

We strongly believe that the main driver for a higher performance of the education system is the quality of teachers. That’s why our majors programs are focussing on developping teachers’ skills.

Sports

We love sports because they provide us with an exciting journey with some beautiful moments, heroes who win, attract new fans or, on the contrary, struggle with difficult moments.

Environment

Economic development is no longer possible without environmental and social progress. It is our responsibility to propose business models that encourage the positive transformation of the world.

The Civil Society

Community involvement is designed to build sustainable intervention mechanisms so that children and young people in difficult situations can develop their skills

Financial Information

Discover

Learn

Apply

The remote banking service provides you with information on your bank accounts directly from your mobile phone.

Find out more »MyBRD Contact is a service which allows you to quickly make your current operations through the phone.

Find out more »Safekeeping, registering, monitoring and controlling the applications for subscription or redemption of fund units.

Find out more »Distribution of fund units, dividends and bond payments. Group distribution services within public offerings.

Find out more »Administration availability of customer accounts to their instructions - financial instruments operations or cash.

Find out more »Clearing services for transactions made on Bucharest Stock Exchange, Bucharest Clearing House and SIBEX.

Find out more »Clearing services for transactions made on Bucharest Stock Exchange, Bucharest Clearing House and SIBEX.

Find out more »News and related materials of our current activity: from business press releases to cultural, educational, sport or technological projects

Find out more »is an online cultural publication that shapes the portrait of the new generation of creators

Find out more »is an editorial project dedicated to the pre-university education created by DoR and BRD

Find out more »Find here our mass media contacts

Find out more »We invest in culture because we need leaders and projects to remind us where we come from, who we are and where we are heading to.

Find out more »We strongly believe that the main driver for a higher performance of the education system is the quality of teachers. That’s why our majors programs are focussing on developping teachers’ skills.

Find out more »We love sports because they provide us with an exciting journey with some beautiful moments, heroes who win, attract new fans or, on the contrary, struggle with difficult moments.

Find out more »Economic development is no longer possible without environmental and social progress. It is our responsibility to propose business models that encourage the positive transformation of the world.

Find out more »Community involvement is designed to build sustainable intervention mechanisms so that children and young people in difficult situations can develop their skills

Find out more »

- Select the card and enter the 3-digit code on the back of the card.

- Tap on the message that will appear in the mobile app.

- Authorise the transaction

- Return to the payment page and confirm payment

Quick and easy. That's why we recommend installing the You mobile app on your phone.

Enter your dynamic password on the payment page as soon as you receive it, as it is only valid for 5 minutes.

✓ make unsecured payments exceeding EUR 30

✓ make more than 5 consecutive unsecured payments on a card or exceed the cumulative amount of €100.

If you have reached these thresholds, you will need to authenticate by biometrics or 2-factor method. There are certain situations where you can make unsecured payments exceeding the above limits. These are payments with a low reported fraud rate, which the merchant decides and assumes to allow in an unsecured manner, following its own analysis by payment type and customer profile.

The attacker sends an SMS or email advising the card user to give their confidential data in order to win certain prizes or informs them that they are needed due to technical errors that led to the loss of the original data. The attacker usually also sends a web address containing a clone of a merchant's or even bank's website.

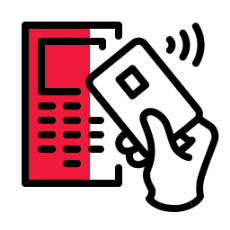

In this type of fraud the attacker impersonates someone else to obtain the data needed to make a payment with the user's card.

Criminals install devices to read the card's magnetic stripe data at ATMs or POS machines. Card data is copied when using the terminal. In the case of ATM data copying, a camera is also installed so that the PIN code can also be stolen.

Attackers use software applications that install malicious code on payment devices without the user's knowledge. The purpose of these apps is to collect data and use it for fraudulent payments.

We send you an SMS to confirm certain transactions that have certain risk criteria, such as categories of merchants where transactions with a high degree of risk are possible, transactions that are out of the pattern of frequently performed transactions and others.

If you text us back that you don't recognise the transaction, we block the card to prevent further fraudulent transactions. If you do not reply within 10 minutes, as a security measure, we will temporarily block your card. You can reply to our message within 24 hours. Confirm or deny the transaction and we will unblock or keep the card blocked, depending on your answer.

After 24 hours, please contact MyBRD Contact to confirm or deny transactions.

We apply high security standards (PCI-DSS).

We monitor transactions through dedicated anti-fraud applications.

We are notifying the authorities to identify the offenders.

We would like to remind you that BRD - Groupe Societe Generale has not requested and will never ask any of your authentication data (user code, password or password token) or confidential information related to your card (card number, expiration date, security code or PIN) by phone, nor e-mail or SMS.

These confidential data will be used only for the internet banking authentication or for online payments.

At the same time, if you notice a different appearance of the usual MyBRD Net application (ex. A notification message that the page is unavailable and you are invited to log in again, or to sync your token device), please stop the authentication process immediately and contact as soon as possible through MyBRD Contact tel: 021 302 6161.